Provisional tax in South Africa applies to all companies and to any individual earning more than R30,000 from non-employment sources — construction contractors, farmers, and equipment owners included. MCM Group explains how the IRP6 system works, when payments are due, and how equipment depreciation reduces your liability, from branches in Cape Town, George, Gauteng, and Bloemfontein.

Provisional tax is SARS’s method of collecting income tax in advance — before you file your annual return. Instead of one large year-end payment, you submit estimated tax payments via IRP6 returns during the tax year itself. Every company must submit, regardless of profit or loss. Individuals whose non-PAYE income exceeds R30,000 per year must also submit. If you own construction equipment, run a contracting business, or operate a farm, provisional tax is not optional.

Planning a new equipment purchase this tax year? Contact MCM Group for full specification sheets, VAT invoices, and finance documentation — everything your accountant needs to structure the depreciation claim correctly.

Who Pays Provisional Tax in South Africa?

Two categories of taxpayers must submit provisional tax returns:

- All companies and close corporations — every company must submit IRP6 returns for each provisional period, regardless of whether it made a profit or a loss. A nil return must still be filed.

- Individuals with non-PAYE income above R30,000 — sole proprietors, independent contractors, farmers, and anyone earning rental income, commission, or directorship fees above this threshold. SARS can also formally notify a taxpayer to submit provisional tax even below the threshold.

If your only income is a PAYE salary, you are generally not a provisional taxpayer. The moment you add an income stream outside PAYE — plant hire, farming income, or subcontracting — the obligation may arise. When in doubt, confirm your status with a registered tax practitioner.

Provisional Tax Payment Dates — IRP6 Deadlines

South Africa’s tax year for individuals runs from 1 March to 28/29 February. For companies with a February year-end, the provisional tax calendar works as follows:

| Payment | Deadline | Who It Applies To |

|---|---|---|

| First period (IRP6 #1) | 31 August | Individuals and companies |

| Second period (IRP6 #2) | 28/29 February | Individuals and companies |

| Third period (voluntary top-up) | 30 September (6 months after year end) | Individuals and companies — optional |

Companies with year-ends other than February shift these dates to align with their own financial year. The pattern is the same: first IRP6 at the 6-month mark, second at year end. An optional third payment follows 6 months after year end. You must submit a nil IRP6 for every period — skipping is not permitted, even when no tax is owed. Failure to submit a nil return is a compliance breach and may affect your tax clearance status.

How to Estimate Your Provisional Tax Correctly

The IRP6 requires an estimate of your total taxable income for the full year of assessment. Your accountant will base this on year-to-date income, projected revenues, and allowable deductions. These include equipment depreciation, wear and tear, and any carry-forward losses. Getting the estimate right matters, because SARS penalises under-estimation.

Two accuracy rules apply, depending on income level:

- Taxable income above R1,000,000: your estimate must reflect at least 80% of your final assessed tax liability. Anything below that threshold triggers an underestimation penalty of 20% of the shortfall.

- Taxable income of R1,000,000 or less: your second period estimate must be at least the greater of (a) 90% of your final tax liability, or (b) the “basic amount” — the tax assessed on your most recently finalised annual return. The basic amount is often the safer anchor when income is uncertain.

Capital gains must also be included in your estimate. Selling a machine, vehicle, or property during the tax year creates a capital gain that forms part of your taxable income. Include it on your IRP6 — it cannot be deferred to the annual return.

Penalties and Interest for Late or Under-Payment

Missing a deadline or under-estimating your income exposes you to three types of charge:

- 10% late payment penalty — charged on the shortfall for the first and second provisional tax periods. This penalty does not apply to the voluntary third period — only interest applies there.

- 20% underestimation penalty — applied to the difference between your estimate and the applicable threshold (80% of final tax for income above R1 million; 90% or the basic amount for income at or below R1 million).

- Interest at the SARS prescribed rate — currently 10.25% per annum from 1 March 2026. Interest accrues from the date payment was due until SARS receives full settlement.

The best way to avoid all three is a monthly-tracking accountant who submits realistic IRP6 estimates. Last-minute guesses are a common cause of penalties. If you took delivery of major equipment during the year, the depreciation allowance can significantly reduce your estimate. Your provisional tax liability drops with it.

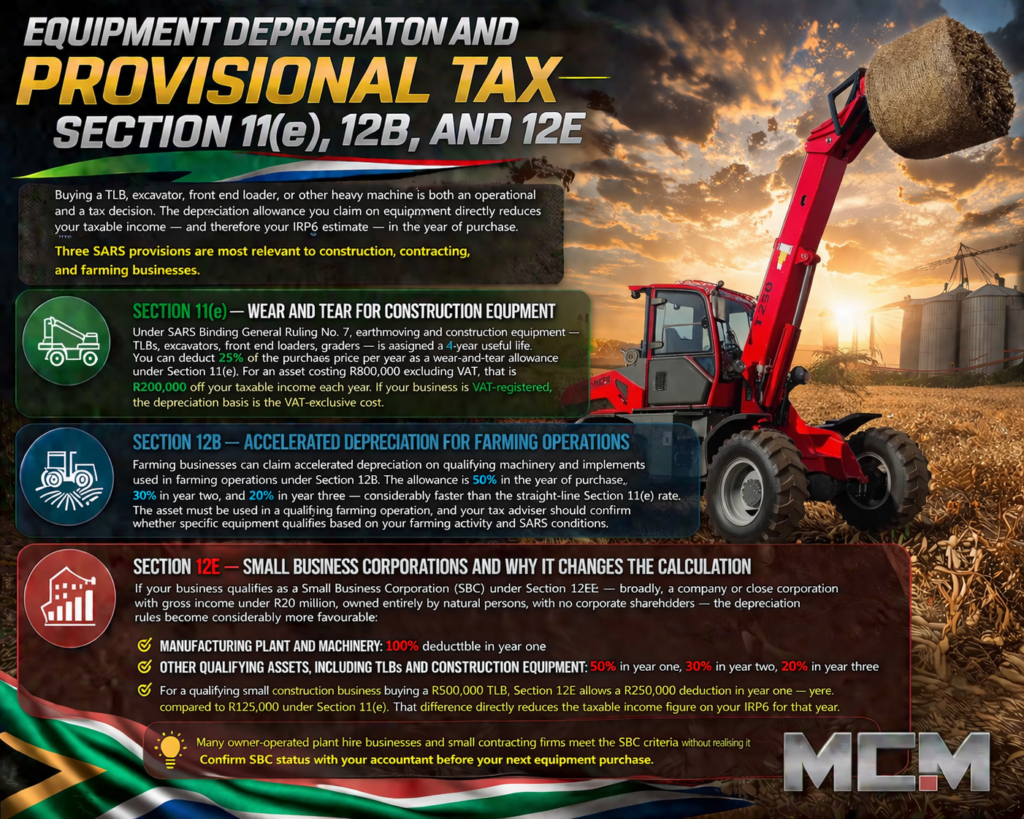

Equipment Depreciation and Provisional Tax — Section 11(e), 12B, and 12E

Buying a TLB, excavator, front end loader, or other heavy machine is both an operational and a tax decision. The depreciation allowance you claim on equipment directly reduces your taxable income — and therefore your IRP6 estimate — in the year of purchase. Three SARS provisions are most relevant to construction, contracting, and farming businesses.

Section 11(e) — Wear and Tear for Construction Equipment

SARS Binding General Ruling No. 7 assigns earthmoving and construction equipment — TLBs, excavators, front end loaders, graders — a 4-year useful life. You can deduct 25% of the purchase price per year as a wear-and-tear allowance under Section 11(e). For an asset costing R800,000 excluding VAT, that is R200,000 off your taxable income each year. If your business is VAT-registered, the depreciation basis is the VAT-exclusive cost.

Section 12B — Accelerated Depreciation for Farming Operations

Farming businesses can claim accelerated depreciation on qualifying machinery and implements used in farming operations under Section 12B. The allowance is 50% in year one, 30% in year two, and 20% in year three. That is considerably faster than the straight-line Section 11(e) rate. The asset must qualify under your farming activity. Your tax adviser should confirm whether specific equipment meets SARS conditions before you claim.

Section 12E — Small Business Corporations and Why It Changes the Calculation

If your business qualifies as a Small Business Corporation (SBC) under Section 12E, the depreciation rules become considerably more favourable. An SBC must have gross income under R20 million, be owned entirely by natural persons, and have no corporate shareholders:

- Manufacturing plant and machinery: 100% deductible in year one

- Other qualifying assets, including TLBs and construction equipment: 50% in year one, 30% in year two, 20% in year three

For a qualifying small construction business buying a R500,000 TLB, Section 12E allows a R250,000 deduction in year one. That is double the R125,000 available under Section 11(e). That difference directly reduces the taxable income figure on your IRP6 for that year. Many owner-operated plant hire businesses and small contracting firms meet the SBC criteria without realising it. Confirm SBC status with your accountant before your next equipment purchase.

Provisional Tax and Tenders — What Non-Compliance Actually Means

Government departments and municipalities require a valid SARS Tax Clearance PIN (TCS PIN) before awarding contracts. Your TCS PIN is only valid when your tax affairs are fully compliant — including current provisional tax submissions and payments.

Being behind on provisional tax does not automatically disqualify you from tendering. It may, however, prevent or delay TCS PIN approval — and that delays tender acceptance and CSD registration. For businesses that depend on municipal or government work, this creates a direct operational risk. Staying current on your IRP6 submissions keeps your compliance status clean and your TCS PIN available on demand. This includes nil returns for every period — even when no tax is owed.

Buying equipment before your next provisional tax deadline? Contact MCM Group for a quote, full spec sheets, and finance documentation — the paperwork your accountant needs to process the depreciation allowance correctly.

Frequently Asked Questions About Provisional Tax in South Africa

What is provisional tax in South Africa and how does it work?

Do I have to submit an IRP6 if I owe no provisional tax?

What is the difference between the first and third provisional tax payment?

Equipment Depreciation and Tax Allowances

How does buying a TLB or excavator reduce my provisional tax bill?

What is a Small Business Corporation and how does Section 12E help equipment owners?

Tender Compliance and Documentation

Will being behind on provisional tax affect my ability to tender?

Where can I get the equipment specs and documentation my accountant needs?

More Common Questions

Does provisional tax apply to sole proprietors and independent contractors?

Is capital gains tax included in the provisional tax estimate?

Sources and References

Disclaimer: MCM Group is a heavy equipment distributor, not a financial institution, tax adviser, or accounting firm. The information in this article is for general informational purposes only and does not constitute tax, financial, or legal advice. Tax laws, SARS prescribed rates, and compliance requirements change regularly — the figures in this article reflect the position as at April 2026 and should be verified with a registered tax practitioner before reliance. Always consult a qualified accountant or CA(SA) before making decisions about provisional tax estimates, depreciation claims, or business structure.

- SARS — Provisional Tax for Individuals

- SARS — Provisional Tax for Businesses and Employers

- SARS — Income Tax Act (Sections 11(e), 12B, 12E)

- SARS Binding General Ruling No. 7 — Wear and Tear Allowances

- South African Institute of Chartered Accountants (SAICA)

Find MCM Group Nationwide

MCM Group has four branches across South Africa. Contact your nearest branch for equipment specifications, VAT invoices, financing documentation, and delivery timelines.

- Cape Town — 7 Jig Avenue, Montague Gardens | +27 (0)21 001 8686

- George — 14 Mellville Street, George Industria | +27 (0)44 873 3355

- Gauteng (Rosslyn, Pretoria) — 28 Brits Road, Rosslyn | +27 (0)12 940 9026

- Bloemfontein — 11 Woodrow Street | +27 (0)51 101 0095

Buying new equipment before your next provisional tax period? The depreciation allowance you claim this year reduces your IRP6 estimate immediately. Contact MCM Group for a quote, full spec sheets, and finance options — the documents your accountant needs to maximise your tax position.