Quick answer

Instalment sale, financial lease and operating lease are the three main ways to finance equipment in South Africa, and each one is designed to allocate ownership, tax deductions and balance-sheet treatment differently.

An instalment sale is an agreement where you own the asset and claim wear-and-tear, a financial lease provides similar long-term benefits, and an operating lease allows you to use a machine without owning it, so the best structure is determined by your tax position.

Best for: contractors and farmers choosing between instalment sale, financial lease and operating lease to fund a machine tax-efficiently.

MCM Group helps South African contractors and farmers choose the right equipment finance structure — instalment sale, financial lease, operating lease, asset finance, or rent to own — with expert guidance from branches in Cape Town, George, Gauteng, and Bloemfontein.

Equipment finance in South Africa comes in several forms: instalment sale (you own it from day one), financial lease (option to buy at the end), operating lease (pure rental), asset finance (security-backed lending where the machine itself is the collateral), and rent to own (rental payments that build toward purchase). Each has different tax, VAT, and balance sheet implications that directly affect your bottom line. Choosing the wrong structure could cost your business tens of thousands of Rands in lost deductions every year — so getting this right matters.

This guide breaks down all three equipment finance options so you can make a confident, informed decision before you sign anything.

How Equipment Finance Works in South Africa

When you need a new excavator, TLB, or tractor, paying cash is rarely the smartest move. Equipment finance lets you spread the cost over 24 to 60 months while you put the machine to work earning income straight away.

Generally, South African businesses access equipment finance through banks like Nedbank, Standard Bank, ABSA, or FNB, as well as specialist asset finance houses. The finance provider buys the equipment (or lends you the money to buy it), and you repay over an agreed term with interest.

In fact, three structures dominate the market. Each one treats ownership, tax deductions, and VAT differently. Your accountant and tax advisor should weigh in — but you also need to understand the basics yourself, because the structure you pick affects your cash flow from month one.

Let’s look at each structure in detail, using an MCM 920 Front End Loader at R450 000 as a working example throughout.

Instalment Sale Agreement — Own It from Day One

An instalment sale agreement (sometimes called hire purchase) is the most common way to finance equipment in South Africa. You take ownership of the asset immediately, even though you pay it off in monthly instalments.

How it works: The finance house pays the dealer. From there, you receive the equipment and start repaying the capital plus interest over your chosen term. As a result, title transfers to you from the start — meaning the asset sits on your balance sheet right away.

Tax treatment: Because you own the asset, you claim capital allowances (wear-and-tear) under SARS rules. For most movable assets used in manufacturing or construction, section 12C of the Income Tax Act allows a 20% straight-line deduction per year over five years. As a result, on a R450 000 MCM 920 Front End Loader, that means R90,000 per year in tax deductions — regardless of what your monthly instalment looks like. Plus, you also deduct the interest portion of each monthly payment.

VAT advantage: Because of this, you claim the full input VAT (15%) upfront in the month you take delivery. Consequently, on a R450 000 machine, that’s a R58 696 VAT claim in month one — a massive cash flow boost if your business is VAT-registered.

Watch out for: If you sell the asset later for more than its tax book value, SARS will recoup the difference. For example, if you sell the MCM 920 after three years when its tax value is R180 000 but you get R300,000, you’ll pay tax on the R120,000 recoupment.

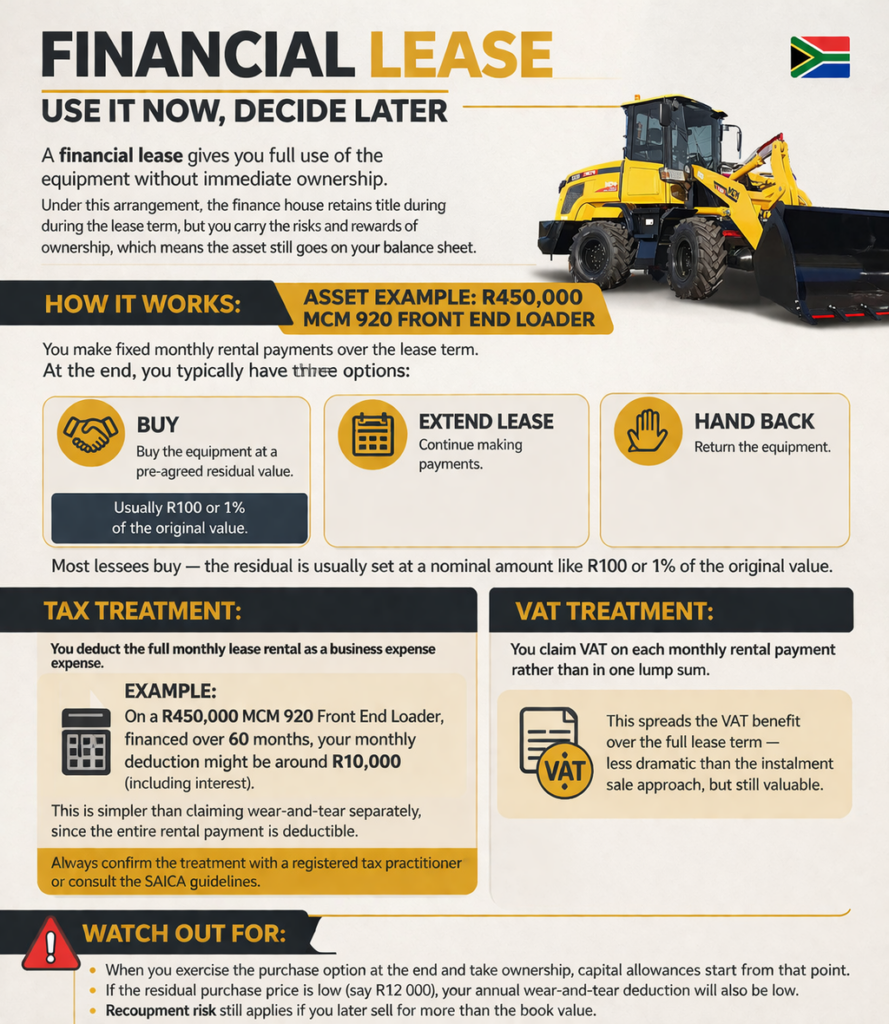

Financial Lease — Use It Now, Decide Later

A financial lease gives you full use of the equipment without immediate ownership. Under this arrangement, the finance house retains title during the lease term, but you carry the risks and rewards of ownership, which means the asset still goes on your balance sheet.

How it works: In practice, you make fixed monthly rental payments over the lease term. At the end, you typically have three options: buy the equipment at a pre-agreed residual value, extend the lease, or hand it back. In practice, most lessees buy — the residual is usually set at a nominal amount like R100 or 1% of the original value.

Tax treatment: Because of this, you deduct the full monthly lease rental as a business expense. Similarly, on our R450,000 MCM 920 Front End Loader, financed over 60 months, your monthly deduction might be around R10,000 (including interest). In practice, this is simpler than claiming wear-and-tear separately, since the entire rental payment is deductible. Above all, always confirm the treatment with a registered tax practitioner or consult the SAICA guidelines.

VAT treatment: In turn, you claim VAT on each monthly rental payment rather than in one lump sum. In practice, this spreads the VAT benefit over the full lease term — less dramatic than the instalment sale approach, but still valuable.

Watch out for: When you exercise the purchase option at the end and take ownership, capital allowances start from that point. If the residual purchase price is low (say R12 000), your annual wear-and-tear deduction will also be low. Similarly, the recoupment risk still applies if you later sell for more than the book value.

Operating Lease — Pure Rental, No Ownership

An operating lease is straightforward: you rent the equipment for a fixed period, and the finance house keeps ownership throughout. Think of it like a long-term rental agreement with no intention to buy.

How it works: Under this structure, you pay a fixed monthly rental. Under this model, the lessor maintains ownership and usually takes on residual value risk. At the end of the term, you return the equipment. Some operating leases include maintenance — making your monthly cost predictable and your budgeting simpler.

Tax treatment: The full monthly rental is a deductible expense against your taxable income. As a result, you claim the entire payment — no depreciation schedules, no capital allowance calculations. It’s the simplest tax treatment of the three options.

Balance sheet benefit: Because you never own the asset, an operating lease keeps the equipment off your balance sheet. As a result, this improves financial ratios like return on assets and debt-to-equity, which matters when you apply for bonds, overdrafts, or tender pre-qualification. Note that IFRS 16 has changed how listed companies report leases, but many SMEs in South Africa still benefit from off-balance-sheet treatment under IFRS for SMEs.

VAT treatment: You claim input VAT on each monthly rental payment. In short, simple and consistent.

Watch out for: Keep in mind that you build zero equity in the equipment. At the end of the lease, you have nothing to show for your payments — no asset to sell or trade in. If you plan to use the machine for 10+ years, renting it for five years and then walking away rarely makes financial sense.

Asset Finance — Using Your Equipment as Security

“Asset Finance” is the term South African banks and finance houses use to describe any lending arrangement where the physical asset itself serves as the primary security for the loan. Unlike an unsecured business loan — which relies on your balance sheet, revenue history, and creditworthiness alone — asset finance means the machine is registered as collateral. The lender holds an interest in the equipment, which reduces their risk and, in turn, makes it easier for South African SMEs and contractors to qualify.

This is the category that sits above both instalment sales and financial leases. When Nedbank offers “Business Equipment Finance”, when WesBank approves an “Asset and Vehicle Finance” deal, or when ABSA processes an “Asset-Based Finance” application, they are all operating within the asset finance framework — just using different contractual structures underneath. The key point for you as a buyer: the equipment you’re purchasing is doing the work of securing the loan, so you need less outside collateral to get approved.

Asset finance typically offers lower interest rates than unsecured lending because the lender can repossess and resell the equipment if you default. For businesses with limited trading history, few free assets, or a lean balance sheet, this security mechanism is often the only viable route to acquiring high-value machinery. MCM Group’s finance team submits applications across multiple asset finance providers simultaneously, so you get the most competitive rate available without approaching each bank separately.

Rent to Own / Rent to Buy — Build Toward Ownership

Rent to own (also called rent to buy) is a dealer-arranged finance structure where you rent equipment for an agreed period, and your rental payments — or a portion of them — contribute directly toward the purchase price. At the end of the rental term, you exercise the option to buy the equipment at the pre-agreed residual, which is lower because your payments have already been building equity. The intended end-point from day one is ownership, which is the critical distinction from an operating lease (where you walk away) and a financial lease (which is bank-arranged and credit-assessed).

How it differs from a financial lease: A financial lease is a formal bank product — it requires full credit assessment, FICA documentation, and the purchase option at the end is typically set at a nominal residual (e.g. R100 or 1%). Rent to own is usually arranged directly through a dealer or specialist equipment rental company, often with more flexible qualification criteria. It suits businesses that may not yet qualify for traditional bank finance — start-ups, sole proprietors with limited credit history, or businesses recovering from a difficult trading period — because the dealer carries more of the approval risk. Terms typically run 12 to 36 months.

Tax treatment: During the rental period, your monthly payments are deductible as a business expense. Once you exercise the purchase option and take ownership, the asset moves onto your balance sheet and you begin claiming capital allowances (wear-and-tear) on the residual purchase price going forward. Keep your rental invoices and the final purchase agreement — SARS will need both if you are ever audited. As always, confirm the exact treatment with your tax practitioner before filing.

Equipment Finance Comparison — Side by Side

This table summarises the key differences between all three structures. Use it as a quick reference when you sit down with your accountant or finance broker.

| Feature | Instalment Sale | Financial Lease | Operating Lease | Rent to Own |

|---|---|---|---|---|

| Ownership | Yours from day one | Yours at end (option to buy) | Never yours — pure rental | Yours after purchase option |

| On Balance Sheet | Yes | Yes | No (for most SMEs) | Yes — once purchased |

| Tax Deduction Type | Capital allowances (wear-and-tear) + interest | Full monthly rental | Full monthly rental | Rental as expense; wear-and-tear after purchase |

| VAT Claim | Full amount upfront | Monthly on each rental | Monthly on each rental | Monthly on each rental |

| Recoupment Risk | Yes — on disposal | Yes — after purchase option | No — you never own it | Yes — after purchase, on disposal |

| Arranged By | Bank / finance house | Bank / finance house | Bank / finance house | Dealer or rental company |

| Best For | Long-term ownership, max upfront VAT | Flexibility, deferred ownership decision | Short-term projects, balance sheet management | Limited credit history, flexible path to ownership |

Which Finance Structure Should You Choose?

There’s no single best answer — the right structure depends on your business goals, tax position, and how long you plan to keep the equipment.

Choose an instalment sale if:

- For example, you want to own the equipment outright at the end of the term

- Your business is VAT-registered, and you want the full VAT claim upfront

- You plan to use the machine for its full economic life (7–15 years)

- You want to build asset value on your balance sheet for tender pre-qualification

Choose a financial lease if:

- You want flexibility to decide on ownership at the end of the term

- You prefer a single monthly deduction rather than tracking depreciation schedules

- Your tax advisor recommends spreading deductions evenly over the lease term

- You’re uncertain whether the equipment will still suit your operation in five years

Choose an operating lease if:

- You need equipment for a specific project or contract with a defined end date

- Keeping assets off your balance sheet improves your financial ratios

- You want predictable monthly costs with no residual value risk

- You prefer to upgrade to newer models every few years without selling old machines

Choose rent to own if:

- Your business is new or you have limited credit history that makes bank approval difficult

- You want to own the equipment at the end but need a more flexible qualification process

- You prefer a shorter commitment (12–36 months) with a clear path to ownership

- You would rather deal directly with a dealer or rental company than go through a bank

How MCM Group Helps You Get Financed

MCM Group doesn’t just sell equipment — the team helps you secure the right finance package for your situation. As a SAFCEC-recognised dealer, MCM works with multiple finance houses to find competitive rates and terms that match your cash flow.

Here’s what the process looks like:

- Identify the right machine — MCM’s product specialists help you match equipment to your job requirements, whether that’s a new Bell ADT or a used CAT excavator.

- Get a finance quote — MCM submits your application to multiple finance houses simultaneously, saving you the legwork of approaching each bank separately.

- Choose your structure — Based on the quotes received, MCM walks you through the instalment sale, financial lease, and operating lease options so you can pick the one that suits your tax and cash flow needs.

- Take delivery — Once approved, MCM handles logistics and handover so you can get the machine on site fast.

This broker-style approach means you’re not locked into a single bank’s rates or terms. MCM’s finance team compares offers from Nedbank, WesBank, Standard Bank, and specialist lenders to give you the best deal available.

Before You Apply — Quick Checklist

Gather these documents before you contact MCM or your finance house. Naturally, having everything ready speeds up approval and shows lenders you’re serious.

- Latest 6 months’ bank statements (business account)

- Most recent annual financial statements (AFS) or management accounts

- CIPC company registration documents (for PTY Ltd companies)

- Certified copy of ID for all directors or members

- Tax clearance certificate or tax compliance pin from SARS

- Proof of business address (utility bill or lease agreement)

- Quote or proforma invoice for the equipment you want to finance

- Details of existing finance agreements (if any)

Sole proprietors should also include three months’ personal bank statements and a letter from their accountant confirming trading history.

Finance It Yourself or Let MCM Handle It

You have two paths when financing construction equipment in South Africa. You can approach a bank or finance house directly, or you can let MCM Group submit your application to multiple lenders on your behalf.

Contact Your Own Bank

If you already have a banking relationship, your bank may offer competitive rates. The major SA banks with dedicated equipment finance divisions include:

- Nedbank — Business Equipment Finance

- WesBank — Asset and Vehicle Finance

- Standard Bank — Business Lending

- ABSA — Asset-Based Finance

- FNB — Business Finance Solutions

Specialist Equipment Finance Providers

Beyond the big banks, specialist asset finance companies focus exclusively on equipment and often offer more flexible terms for contractors and farmers:

- The Rental Company — Asset funding and rental financing for specialist equipment across South Africa, with offices in Johannesburg, Cape Town, Port Elizabeth, and Bloemfontein. They offer fast payouts, competitive rates, and minimal paperwork.

Let MCM Group Arrange Your Finance

The easiest route is to let MCM Group handle your finance application. MCM acts as a broker, submitting your application to multiple banks and finance houses at the same time. You get competing offers without filling in separate applications, and MCM walks you through the options so you choose the best structure for your business.

Contact MCM Group to start your equipment finance application today. The process takes minutes, and most applications receive a decision within 48 to 72 hours.

Your Questions Answered

What is the difference between an instalment sale and a financial lease?

Can I claim VAT on construction equipment finance?

Which finance option keeps equipment off my balance sheet?

How long does equipment finance approval take in South Africa?

What is the difference between rent to own and a financial lease?

More Common Questions

What documents do I need to apply for equipment finance?

Does MCM Group offer equipment finance?

Can a sole proprietor apply for equipment finance?

About the Author

Disclaimer: MCM Group is an equipment distributor, not a financial institution or registered financial services provider. The information in this article is for general informational purposes only and does not constitute financial, tax, or legal advice. Always consult a qualified accountant, registered tax practitioner, or financial advisor before making decisions about equipment financing, tax deductions, or lease structures. Terms, rates, and eligibility criteria are determined by the relevant bank or finance house.

Sources & References

- SAICA — Lease and Suspensive Sale Finance

- SAICA — Financial Leases: Income Tax and VAT

- SAIT — Income Tax Implications of Finance Leases

- PWC South Africa — Corporate Deductions

- SAFCEC — South African Forum of Civil Engineering Contractors

Find Us Nationwide

MCM Group has branches in Cape Town, George, Gauteng (Midrand), and Bloemfontein. Walk in, call, or get in touch online for equipment advice, finance guidance, and after-sales support.

Why buyers trust MCM Group

MCM Group has supplied and serviced construction and agricultural equipment across all nine South African provinces since 2008. Every machine is backed by a local warranty, a National Parts Division and technical support from four branches in Cape Town, George, Bloemfontein and Midrand.