Submitting an equipment finance application in South Africa is easier when you know what banks look for. MCM Group works with multiple banks and finance houses on your behalf — helping contractors and farmers secure competitive rates on TLBs, front end loaders, excavators, and more, from branches in Cape Town, George, Gauteng, and Bloemfontein.

Equipment finance in South Africa lets you spread the cost of machinery over 24 to 60 months while keeping cash flow intact. Banks and finance houses assess your creditworthiness, business financials, and the asset itself before approving your application — and knowing what they look for gives you a real advantage.

Need help with your equipment finance application? Contact MCM Group — we submit to multiple lenders on your behalf and help you find the best deal.

What Banks Check Before Approving Equipment Finance

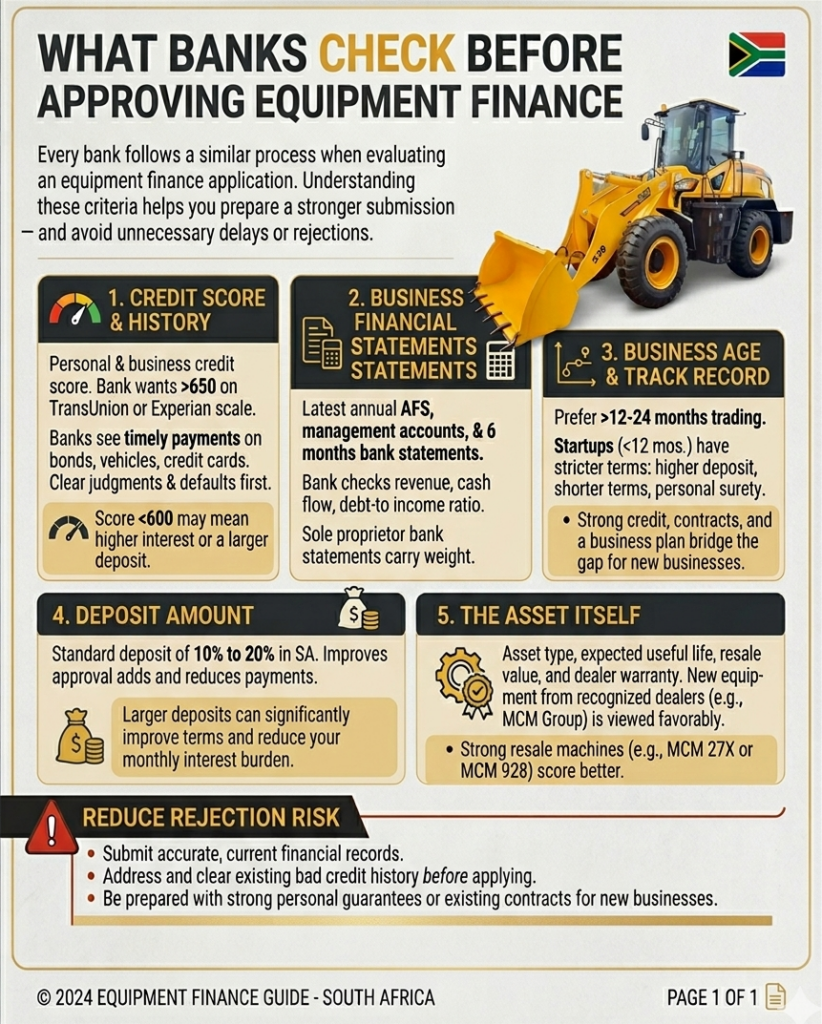

Every bank follows a similar process when evaluating an equipment finance application. Understanding these criteria helps you prepare a stronger submission — and avoid unnecessary delays or rejections.

1. Credit Score and Payment History

Your personal and business credit score is the first thing a lender checks. A score above 650 on the TransUnion or Experian scale generally puts you in a good position. Banks want to see that you pay your existing obligations on time — bond repayments, vehicle finance, credit cards, and supplier accounts all count.

If your credit score is below 600, you may still qualify through asset-based lending, but expect a higher interest rate or a larger deposit requirement. Clearing judgments and paid-up defaults before applying makes a measurable difference.

2. Business Financial Statements

Banks typically request your latest annual financial statements (AFS), management accounts, and six months of business bank statements. They want to see consistent revenue, positive cash flow, and a debt-to-income ratio that leaves room for the new instalment.

For sole proprietors and smaller contractors, bank statements often carry more weight than formal AFS — because they show real-time cash movement. Make sure your business account reflects healthy turnover and minimal returned debits in the months before you apply.

3. Business Age and Track Record

Most banks prefer businesses that have been trading for at least 12 months. Some require 24 months. Startups under 12 months can still access equipment finance, but the terms are usually stricter — higher deposits, shorter repayment periods, or personal suretyship requirements.

If your business is new, showing a strong personal credit record, existing contracts or tenders, and a clear business plan helps bridge the gap.

4. Deposit Amount

A deposit of 10% to 20% of the asset value is standard for equipment finance in South Africa. Some lenders offer zero-deposit deals for applicants with excellent credit and strong financials — but a deposit always improves your approval odds and reduces your monthly repayment.

On a machine like the ACE Phantom TLB, a 10% deposit means roughly R90,000 upfront. That lowers your financed amount and saves you thousands in interest over the term.

5. The Asset Itself

Banks assess the equipment you want to buy — not just your ability to pay. They look at the asset type, the expected useful life, resale value, and whether it comes from a recognised dealer with warranty support. New equipment from an established distributor like MCM Group is viewed more favourably than used equipment from a private seller.

Machines with strong resale markets — like the MCM 27X TLB or the MCM 920 Front End Loader — also score well because the bank knows it can recover value if the deal goes wrong.

How MCM Group Makes Equipment Finance Easier

MCM Group acts as a finance broker rather than a single-source lender. When you request finance through MCM, your application goes to multiple banks and finance houses simultaneously — including Nedbank, WesBank, Standard Bank, and specialist asset finance providers.

This broker approach means you get competing offers without submitting separate applications to each bank. MCM’s finance team compares the rates, terms, and conditions, then walks you through the options so you can choose the structure that suits your business best.

What Documents You Need for Equipment Finance

- The latest 6 months’ business bank statements

- Most recent annual financial statements or management accounts

- Certified copy of ID (directors/members)

- Proof of business address

- Company registration documents (CIPC)

- Tax clearance certificate or TCS PIN

- Latest SARS returns (income tax and VAT)

- Details of existing finance obligations

Having all documents ready before you submit your equipment finance application speeds up the process significantly. Most equipment finance applications receive a decision within 48 to 72 hours when documentation is complete.

Tips to Improve Your Equipment Finance Approval Chances

- Clear any outstanding judgments or defaults before applying

- Keep your business bank account in good standing — avoid returned debits for at least 3 months before the application

- Offer a deposit of at least 10% — it shows commitment and reduces the bank’s risk

- Buy from a recognised dealer with warranty and parts support — banks prefer this over private sales

- Apply through a broker like MCM Group who submits to multiple lenders — this gives you more options without multiple credit checks

- Match the finance term to the machine’s working life — a 5-year term on equipment you plan to use for 10 years is a strong position

Your Questions Answered

What credit score do I need for equipment finance in South Africa?

Can a new business apply for equipment finance?

How long does equipment finance approval take?

More Common Questions

What financing options does MCM Group offer?

Do I need a deposit for equipment finance?

Can I finance used construction equipment?

Sources & References

Disclaimer: MCM Group is an equipment distributor, not a financial institution or registered financial services provider. The information in this article is for general informational purposes only and does not constitute financial, tax, or legal advice. Always consult a qualified accountant, registered tax practitioner, or financial advisor before making decisions about equipment financing, tax deductions, or lease structures. Terms, rates, and eligibility criteria are determined by the relevant bank or finance house.

- Nedbank — Business Asset Finance

- WesBank — Equipment Finance

- Standard Bank — Vehicle and Asset Finance

- SAFCEC — South African Forum of Civil Engineering Contractors

Find Us Nationwide

MCM Group has branches in Cape Town (Montague Gardens), George, Gauteng (Rosslyn, Pretoria), and Bloemfontein. Walk in, call, or get in touch online for equipment advice, finance assistance, and competitive quotes.