MCM Group supplies construction and agricultural equipment across South Africa — and understanding how VAT applies to your purchase can save your business tens of thousands of rands. Whether you buy a TLB, front end loader, or excavator, MCM branches in Cape Town, George, Gauteng, and Bloemfontein provide full tax invoices so you can claim your input VAT without hassle.

VAT on construction equipment in South Africa sits at the standard rate of 15%. If your business is VAT-registered and uses the equipment for taxable supplies, you can claim the full VAT amount back as an input tax credit. You do this through your VAT 201 return — putting significant money back into your cash flow.

Ready to get a tax invoice and start your input VAT claim? Contact MCM Group for a quote on any machine in our range.

Understanding VAT on Equipment Purchases

South Africa’s Value-Added Tax Act (Act 89 of 1991) requires vendors to charge VAT at 15% on most goods and services. For example, when you buy an ACE Phantom TLB at R900,000 excluding VAT, the supplier adds R135,000 in VAT. As a result, your total comes to R1,035,000.

However, that R135,000 is not a sunk cost if your business holds a VAT registration. You claim it back as input tax on your next VAT return. SARS then processes the claim as part of your regular VAT cycle. The money comes back to you as either a reduced VAT liability or a direct refund.

In other words, the input VAT claim on that ACE Phantom TLB is R135,000 (R900,000 × 15%, or equivalently R1,035,000 × 15/115). That amount can fund fuel, wages, or a deposit on additional equipment.

Who Can Claim Input VAT on Equipment

Not every business qualifies for an input VAT claim. To succeed, you must meet all three of these requirements:

- VAT registration: Your business must hold a VAT registration with SARS. Currently, compulsory registration applies when taxable supplies exceed R1 million per year. From 1 April 2026, this threshold increases to R2.3 million. Similarly, voluntary registration is available from R50,000 per year, rising to R120,000 from 1 April 2026.

- Taxable purpose: You must use the equipment to make taxable supplies. In practice, this means you charge VAT on the services you provide using the machine. For example, construction services, earthworks, transport, and farming activities generally qualify — provided your business charges VAT on those supplies.

- Valid tax invoice: You need a proper tax invoice from the supplier. It must show the supplier’s VAT number, the amount of VAT charged, and a description of the goods. MCM Group issues compliant tax invoices on every sale.

Additionally, if you use the equipment partly for taxable and partly for exempt or non-business purposes, you can only claim the portion that relates to taxable use. SARS calls this an apportionment. You must apply it consistently.

When to Claim Your Input VAT

Timing matters. On the invoice basis of accounting, you deduct input VAT in the tax period during which the supply takes place. However, you must also hold the required documentary proof — specifically, a valid tax invoice. In practice, this usually aligns with the period in which the equipment arrives and the supplier issues the invoice.

For instance, if your VAT periods run January–February and you take delivery of an MCM 37X TLB on 15 February, you include the claim in that period’s VAT 201 return.

Late Claims and the Five-Year Window

SARS generally allows claims or revisions within five years from the date the tax became chargeable. Nevertheless, you should claim as early as possible. Delayed claims attract SARS scrutiny and may complicate your VAT reconciliation.

Claiming VAT on Financed Equipment

If you finance the equipment through an instalment credit agreement (which most equipment finance deals use), the full input VAT is claimable in the period of delivery. You do not spread it over the finance term. This is a critical point that many contractors miss. Even though you pay monthly instalments over 60 months, the VAT claim happens once — at delivery.

Zero-Rated vs Standard-Rated Supplies

Construction equipment in South Africa carries the standard rate of 15%. There is no zero-rating or exemption for machinery, regardless of the industry you work in.

By contrast, zero-rated supplies (taxed at 0%) apply to specific categories. These include basic foodstuffs, fuel levy goods, exports, and certain agricultural inputs. However, construction equipment does not fall into any of these categories.

There is one exception worth noting: if you export equipment, the sale may qualify for zero-rating at 0% VAT. But this only applies if you meet the specific documentary and export-route requirements in the VAT Act. If delivery takes place in South Africa, you must generally charge VAT at 15% — unless the regulations for direct or indirect exports apply. Therefore, specialist advice is essential for cross-border transactions.

Common VAT Mistakes When Buying Equipment

SARS audits on equipment VAT claims happen more often than you might expect. Below are the mistakes that trigger rejections or penalties.

Invoice and Registration Errors

- Missing or invalid tax invoices: A proforma invoice, quote, or delivery note does not count as a tax invoice. The document must state “Tax Invoice” and include the supplier’s VAT number, your name and VAT number (for amounts above R5,000), a full description of the goods, and the VAT amount.

- No VAT registration at the time of purchase: You cannot retrospectively claim input VAT on goods you bought before your registration date. The only exception is the section 18(4) adjustment on capital goods still on hand at registration.

- Duplicate claims: Some businesses accidentally claim the same invoice twice — once at order and once at delivery. SARS cross-references invoices, so duplicate claims result in penalties plus interest.

Apportionment and Second-Hand Goods Errors

- Claiming VAT on private-use equipment: If you buy a front end loader and use it on your personal property 30% of the time, you can only claim 70% of the input VAT. Failing to apportion correctly raises a red flag for SARS.

- Misunderstanding used-machine purchases from non-vendors: Buying a used machine from a non-vendor is more nuanced than many people realise. While the seller does not charge VAT, you may still claim a notional input tax deduction (calculated as 15/115 of the purchase price) under the second-hand goods provisions of the VAT Act. However, this only applies if you hold the required documentation — including the seller’s identity details and a signed declaration — and you have made payment. The 2026 Budget introduced stricter timing rules for these claims. As a result, you should consult a registered tax practitioner before relying on this provision.

Record Keeping for VAT on Equipment

SARS requires you to keep all VAT transaction records for a minimum of five years. Specifically, for equipment purchases, you should retain:

- The original tax invoice from the supplier

- Proof of payment (bank statement or EFT confirmation)

- The finance agreement (if applicable)

- Delivery documentation confirming receipt of the machine

- Any apportionment calculations for mixed-use equipment

- Your VAT 201 return showing the input claim

Store these documents both digitally and in hard copy. If SARS requests verification three years later, you need to produce the full paper trail without delay.

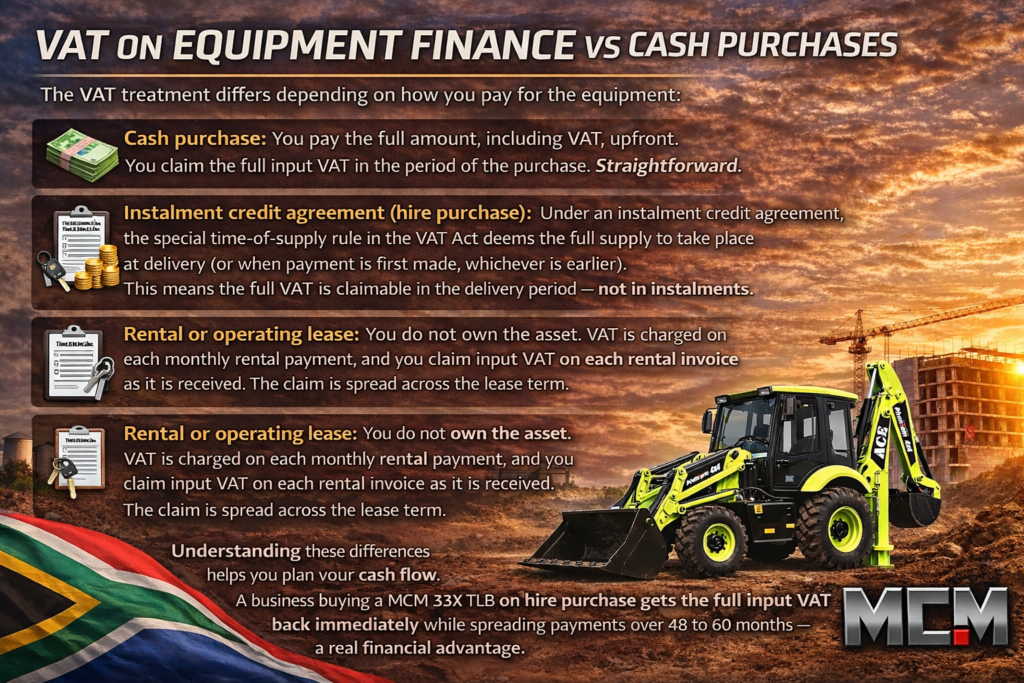

VAT on Equipment Finance vs Cash Purchases

The VAT treatment differs depending on how you pay for the equipment. Here is how each option works.

Cash purchase: You pay the full amount including VAT upfront. You then claim the full input VAT in the period of the purchase. This approach is straightforward.

Instalment credit agreement (hire purchase): Under this arrangement, the VAT Act’s time-of-supply rule deems the full supply to take place at delivery (or when you make the first payment, whichever comes first). As a result, you claim the entire input VAT in the delivery period — not in instalments. This gives you a significant cash flow advantage: the VAT refund arrives in month one, while you pay the machine off over years.

Rental or operating lease: You do not own the asset. Instead, the lessor charges VAT on each monthly rental payment. You then claim input VAT on each rental invoice as you receive it. Consequently, the claim spreads across the lease term.

Understanding these differences helps you plan your cash flow. For example, a business buying a MCM 33X TLB on hire purchase gets the full input VAT back immediately, while spreading payments over 48 to 60 months.

Selling or Trading In Equipment — Output VAT

When you sell equipment on which you previously claimed input VAT, you must charge output VAT at 15% on the selling price. This applies whether you sell to another business or trade the machine in as part of a new purchase.

For instance, if you trade in your old TLB at R400,000 when buying a new MCM excavator, VAT applies to the trade-in value. The dealer accounts for this in the transaction, and the net VAT position flows through both parties’ VAT returns.

In addition, scrapping, writing off, or otherwise disposing of equipment may trigger a VAT adjustment if you previously used the goods for taxable supplies. The rules depend on the specific circumstances of the disposal. Therefore, always consult your accountant or tax practitioner before disposing of high-value assets.

Your Questions Answered

Can I claim VAT on construction equipment if I am not VAT-registered?

Do I claim the full VAT when I finance equipment?

What documents does SARS need for a VAT claim on equipment?

Is construction equipment zero-rated for VAT in South Africa?

Can I claim VAT on a used machine bought from a private seller?

What happens to VAT when I sell or trade in equipment?

Sources & References

Disclaimer: MCM Group is an equipment distributor, not a financial institution or registered financial services provider. The information in this article is for general informational purposes only and does not constitute financial, tax, or legal advice. Always consult a qualified accountant, registered tax practitioner, or financial advisor before making decisions about equipment financing, tax deductions, or lease structures. Terms, rates, and eligibility criteria are determined by the relevant bank or finance house.

- SARS — Value-Added Tax Overview

- SARS — Budget 2026 FAQs

- SARS — VAT 404 Guide for Vendors

- SARS — VAT Rate FAQs

- PwC Tax Summaries — South Africa Corporate Other Taxes

Find Us Nationwide

MCM Group has branches in Cape Town (Kraaifontein), George, Gauteng (Midrand), and Bloemfontein. Walk in, call, or get in touch online for equipment advice, VAT-compliant tax invoices, and competitive quotes.